Best Ways to Invest $10,000

Ad Disclosure: This article contains references to products from our partners. We may receive compensation if you apply or shop through links in our content. This compensation may impact how and where products appear on this site. You help support CreditDonkey by using our links.

Discover 15 savvy ways to make your $10k grow. This expertly curated guide will help you maximize your returns.

|

What would you do if someone handed you $10,000? Would you go on a shopping spree, put it in a savings account, or contribute to the latest trendy investment?

Before you decide, consider your options.

- Try out Real Estate Crowdfunding

- Open a High-Yield Savings or Money Market Account

- Open a Roth IRA

- Invest in Stocks, Mutual Funds, or Bonds

- Start your dream business

The goal is to grow $10,000 over time. To do that, it's essential to develop a solid plan. This will help raise the odds of making the initial amount even bigger.

Trustworthy advice and first-hand experience can make a big difference. So, let's get started on finding the best approach for turning $10,000 into more. (And if $10,000 is too steep for your current situation, find great tips to invest $100.)

Below are some ideas on how to make the most of your $10k.

- Invest in Real Estate

- Invest in Stocks

- Invest in Mutual Funds or Exchange-Traded Funds (ETFs)

- Use a Robo-Advisor for Automatic Investing

- Invest in Bonds

- Try Fulfillment by Amazon

- Start Your Own Business

- Invest in Peer-to-Peer Lending

- Open a CD Account

- Open a Savings Account

- Invest in Yourself

- Fix Up Your Home

- Start a Blog

- Start a Podcast

- Invest in Cryptocurrency

Tip: If you're looking for a passive investment with good long-term profits, investing in real estate is one of the best moves you can make. Fundrise is a great way for beginners to get into real estate because they automatically invest in properties for you. Click here to see their current promotions.

Invest in Real Estate with $10+

- Only $10 minimum investment

- Get a diversified portfolio of real estate projects across the US

- Open to all investors

Free Checking Account for Small Business Owners

- Sign up in 3 minutes; no credit check

- No account fees - $0 monthly fee, overdraft fee, foreign transaction fee, or ATM fees at approximately 40,000 locations

- Automatic Savings

- Get paid up to 2 days early

- Savings with up to 4.00% APY

15 Investment Ideas to Invest $10,000

|

You've set goals and timeframes, lowered your debt, and funded the proper retirement accounts. Now it's time to try making some money.

Here are some great options for investing $10,000, starting with the ones that can offer great returns—but also some risk.

1. Earn Passive Income with Real Estate

Real estate investing is known for being consistently profitable. Over the last 30 years, real estate performed better on average than stocks. That's why it's a favorite among the wealthy.

Luckily, it's not just for millionaires. You can get started with a minimum investment of just $10.

Fundrise lets you pool funds with other investors to purchase real estate. It automatically invests in a variety of real estate properties for you across the US, including residential, commercial, and industrial projects.

The platform takes care of the acquiring, building, and managing of properties. It's a great choice for beginners who want to invest in real estate without dealing with tenants, maintenance repairs, and other headaches.

Fundrise averaged 7.31% returns in 2020 and 22.99% returns in 2021.[1] If you have $10,000 to start, you can get access to more sophisticated strategies with the potential for higher returns.

Start investing in real estate with Fundrise>>

Invitation Program - Up to $100 Share Bonus

Earn up to $100 share bonus for each friend who successfully joins Fundrise through your unique referral link.

2. Invest in Stocks

You don't need a human stock broker to trade stocks. Today, you can use an online brokerage account instead.

Take time to learn about the companies and stocks you're interested in. You can read news, stock performance histories, and professional forecasts. Then, pick one or two stocks to start your investment.

Once you have the basics down, it's time to make a plan. Set an amount of money that you want to invest—and the threshold for how much you're willing to lose.

This way, you remove the emotion involved in investing and avoid making hasty decisions if you see your investments plummeting.

J.P. Morgan Self-Directed Investing - Get Up to $1,000

- Get a cash bonus up to $1,000 when you open and fund a J.P. Morgan Self-Directed Investing account.

- $1,000 when you fund with $250,000 or more

- $325 when you fund with $100,000-$249,999

- $150 when you fund with $25,000-$99,999

- $50 when you fund with $5,000-$24,999

- Get the best of banking and investing on the Chase Mobile® app or Chase.com.

- Choose from stocks, ETFs (from index funds to cryptocurrency), options, mutual funds, money market funds, treasuries and more.

- Get unlimited commission-free online trades.

- Choose an account that's right for you: General Investing, Traditional IRA, Roth IRA, Trusts, or UTMA

- Access our secure, easy-to-use trading experience online or through the Chase Mobile® app.

- Our powerful tools and resources are built to help you take control of your investments.

- Rollover your retirement accounts and keep track of your investments in one place.

- Invest in S&P 500 and Nasdaq 100 stocks, or ETFS, from just $5 - trade from 7:30 AM to 5:45 PM ET for added convenience

INVESTMENT AND INSURANCE PRODUCTS ARE:

Stock Advisor - $99/year for New Members

*$99 is an introductory price for new members only. 50% discount based on current list price of Stock Advisor of $199/year. Membership will renew annually at the then-current list price.

3. Invest in Mutual Funds or ETFs

Mutual funds and ETFs offer diversification. Rather than investing in one company as with stocks, they diversify between stocks, bonds, and other short-term investments. They can invest in many securities all at once.

First, choose a brokerage. Charles Schwab, Vanguard, and Fidelity are among some of the most popular mutual fund companies. See How to Invest Money for more detail.

Longer-term goals, such as retirement, do well with index funds. These funds mimic a specific index, such as the S&P 500. They offer diversification and a long-term investment strategy. The returns on index funds closely mimic market returns. They require little management and often have lower fees.

Mark Kantrowitz, Saving For College

4. Try a Robo Advisor

If you think $10,000 isn't enough for a financial advisor to take you on as a client, consider a robo advisor. A robo advisor is an automated advisor - really, a software program - that does the work for you.

5. Invest in Bonds

Buying a bond is basically just buying debt. You can invest in them much like you would stocks (for the differences between stocks and bonds, read our guide).

Overall, bonds tend to be more predictable than stocks. There are three main types:[2]

- Corporate, which are offered by corporations looking to raise capital

- Municipal, which are issued by towns, cities and states to fund public projects

- Treasury, or T-bonds, which can be purchased directly from the U.S. government

Bonds also receive different ratings based on the credit of the issuer. Typically, you can calculate your return BEFORE you purchase a bond based on rate and period of maturity.

But as with any investments, bonds do carry some risk. For example, when interest rates rise, bond prices fall. This means that if you choose to sell a bond before its maturity date, you could make less than the price you paid for it.

Bonds generally must be purchased through a broker though T-bonds can be bought directly from the government.

6. Try Fulfillment by Amazon

Fulfillment by Amazon is like other selling sites, but easier. You supply the items you sell, but you ship them to Amazon.

You market the products on Amazon's website. Once sold, Amazon ships the items for you. It's the simplest form of selling products online. You don't need coding, graphic design, or social media experience for success.

You'll have access to Amazon's large marketplace of buyers, and you only do a fraction of the work involved with other selling sites. It almost provides immediate gratification.

You can sell new or used items. You can also choose between the individual account (a free account) and the professional account ($39.99 per month).

7. Start Your Own Business

If you are tired of the 9-to-5 grind and want to answer to no one but yourself, this could be your chance. But you'll need a great idea—and a solid business plan—before seriously considering starting your own business.

Unless you have a lot of experience in the industry, make sure you get the help necessary to help you succeed. We recommend visiting the Small Business Administration's website before starting. They offer many resources and steps for beginners and even the experienced business owner.

Starting a business will usually have some upfront costs, even if it's just a small home business. You may have to make a website, hire a logo designer, get supplies, purchase equipment, etc. It's important to keep track of all your expenses - they're tax deductible, after all!

To help separate your business expenses, open a separate business checking account. There are many free ones so you don't need to worry about paying a fee. Some accounts, like Bluevine, even pay interest to help you grow your business funds.

Free Business Checking - Earn $500 Bonus

To earn the $500 bonus, customers must apply for a Bluevine Business Checking account anytime between now and 09/30/2026 using the referral code CD500.

After opening your account, deposit a total of $5,000 within the first 30 days. After 30 days, maintain a minimum daily balance of $5,000 while also completing at least one of the following eligibility requirements every 30 days for 90 days:

- Deposit at least $5,000 from eligible merchant services to your Bluevine account OR

- Make at least $5,000 of outbound payroll payments from your Bluevine account using eligible payroll providers OR

- Spend at least $2,000 on eligible transactions with your Bluevine Business Debit Mastercard® and/or Bluevine Business Cashback Mastercard®

Banking services provided by Coastal Community Bank, Member FDIC

8. Give Peer-to-Peer Lending a Shot

Peer-to-peer (P2P) lending is a somewhat new method of investing. It's a good choice for investors who don't want to deal with a financial institution. Instead, you become the lender. By joining a P2P platform, you can connect with borrowers all over the world.

The benefits of P2P lending are the high rate of return and lower risk.

As an investor, you may pay an origination fee, closing fee, or an annual fee. They work as the intermediary between you and the borrower. They fund the loans (after you pay them), collect payments, and help with litigation should the borrower default.

You can diversify your risk by lending money to multiple borrowers at once. Your $10,000 could fund many borrowers with low borrowing needs.

Keep reading for some low (or no) risk investment ideas you don't want to miss.

|

9. Look at CD Rates

If you are looking for a risk-free investment with decent returns, look at CDs (Certificate of Deposit). We recommend using an online bank rather than a traditional bank. They tend to offer higher rates.

Pro Tip: A popular option to consider is CIT Bank. They provide a selection of CD rates and terms to choose from that help your savings grow.

CIT Bank No Penalty CD - 3.90% APY

- Option to withdraw full balance and interest after 7 days of CD funding date

- $1,000 minimum to open an account

- 11 months

- No monthly maintenance fee

- Member FDIC

CD Rates - Up to 3.50% APY

- $500 minimum opening deposit

- FDIC insured

| Term | CD Rates |

|---|---|

| 6 Month | 3.50% APY |

| 12 Month | 3.50% APY |

| 24 Month | 3.15% APY |

| 36 Month | 2.85% APY |

| 60 Month | 2.75% APY |

10. Fill a Savings Account

When we talk about savings accounts, we don't mean the account at your local bank where you have a checking account. They probably offer measly returns. Instead, look at online savings accounts, where you could obtain rates as much as 10 times higher than your local bank.

CIT Bank's savings account offers one of the highest APYs in the nation (read our review). Take a look at our CIT promo code page to learn more.

You should consider a few things before you invest. Make sure the bank is FDIC insured. Also, read the fine print regarding withdrawals. Make sure you have access to your money when you need it. Some banks may charge fees for withdrawals.

Check for required account minimums too. If you prefer a debit card, look for banks that offer this service.

CIT Bank Platinum Savings - 4.10% APY Boost

| Tier | Boost APY |

|---|---|

| Balance over $5,000 | 4.10%* |

| Balance less than $5,000 | 0.60%* |

After boost is completed, you will continue to earn our best standard rates:

| Tier | APY |

|---|---|

| Balance over $5,000 | 3.75%1 |

| Balance less than $5,000 | 0.25%1 |

- Needs to use promo code to qualify: CITBoost

- Boost lasts 6 months over standard APY

- Tiered account

- $100 minimum account opening

- Member FDIC

- No Monthly Service fees

- No account opening fees

11. Invest in Yourself

Did you ever think of investing in yourself? You could:

- Take online courses

- Go back to school full-time

- Hire a personal coach

Or you could find other ways to better yourself. No matter which avenue you take, you'll gain new knowledge and skills.

You can then take these skills out into the world and make money. They may provide new opportunities for employment, especially if you add a designation to your title.

Certain designations offer you the opportunity to be listed in online directories, such as a CPA. This may result in more business and earnings for you. It's also a great way to enter a new industry. The money can help you make smarter decisions, try new opportunities, and make more money.

That number jumps to $78,000 for those with master's degrees. Salaries vary significantly by industry, however.

12. Fix Up Your Home

Your home may be your largest investment. If it's outdated or needs a facelift, certain improvements can have a direct impact on your home's value.

You don't need to make drastic changes to see a large improvement in value. In fact, major bathroom and kitchen remodels often don't have a large return on investment. New siding, new roof, and new windows often pay off better.

Small changes within the kitchen or bathroom, such as the addition of granite countertops, often pay off.

Another change with a large ROI is updating the home's curb appeal. You may even get bonus points for energy efficient changes you make. Depending on the tax year, you may get a tax break for the new changes made.

But keep in mind, you don't want to wrap up too much of your investment capital in your home. If you need cash, you can't just sell your living room. It's a good idea to have a diversified strategy overall.

Home improvements can add even more value to your property.

13. Start a Blog

If you have a passion for the DIY, consider starting a blog. Many people use this as a side gig. They write when they have time and become affiliate partners with businesses to make money.

Starting a blog won't cost $10,000, but having some capital helps. For starters, you can further your education before starting. Take classes on starting a blog or get in-depth training in your chosen industry. The more you have to talk about, the better, so education helps.

You'll also need money for the domain name, platform, and website hosting. You may also need to upgrade your computer equipment, camera, microphone, and video equipment.

14. Start a Podcast

If writing isn't your thing, but you love to talk, consider starting a podcast. It works like a blog, but you don't host a website. You will need equipment and a host for your podcast, though.

When you first start, your free website may offer enough support. As you gain more followers, you may need greater capabilities. Too many listeners can cause glitches in your podcast. This could be bad for your following.

Today, SoundCloud and Amazon S3 top the charts in podcast hosting. No matter which you choose, read the fine print. Some services, including Amazon S3, charge a base fee, but it increases as your following increases.

Just like a blog, though, you can monetize your podcast. You can sell advertising time within the podcast or let a company advertise on your host page. This can help you afford the podcast hosting fees.

15. Invest in Cryptocurrency

There's a lot of talk around cryptocurrency these days. But investing in crypto comes with high risk.

If you are more technically inclined, crypto mining is a potentially lucrative investment that may recoup your startup costs in less than a year. In case you're unfamiliar, mining is the method by which certain cryptocurrencies like Bitcoin are created.

Miners use their computers (usually dedicated machines that you'll have to spend several thousand dollars on in order to get started) to solve cryptographic puzzles in exchange for rewards paid in the currency they're creating.

With mining, the initial investment is high to be sure, but the rewards (along with risk) are potentially high as well.

Get a $100 Funding Bonus

Sign up through our exclusive CreditDonkey link and fund a new iTrust IRA, a Premium Custody Account (PCA) or a Treasury Account with a minimum of $1,000 to qualify. You must become a New iTrust Customer to be eligible for the Funding Bonus. Terms and conditions apply.

Watch Out! What to Consider Before Investing

|

Before that money burns a hole in your pocket, consider your goals and timeframe. Are you going to need to use it anytime soon? If so, avoid putting it somewhere that's too risky, especially if you might need it in the short-term.

Read on to learn what you should consider.

- Start with Your Goals

What do you dream of doing with your $10,000? Will it fund a luxurious vacation, help you retire, or buy a house? First, categorize your goals as being long-term (retirement) or short-term (vacation).Determine the Time Frame

Divide your goals into categories:- Less than 1 year = short-term goals

- 1-5 years = intermediate goals

- Greater than 5 years = long-term goals

These timelines dictate the level of risk you may want to take. Here's a basic rule: The shorter the timeframe, the less risk you can take. The longer the timeframe, the more risk you may be able to handle.

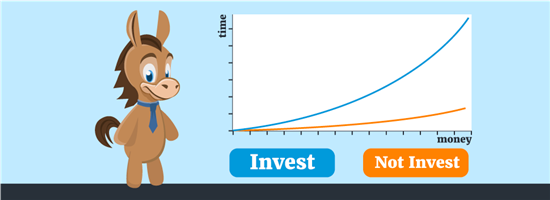

Riskier investments tend to have more ups and downs. Do you have time to ride them out - and perhaps get a greater return? It's a key question for every investment you make.

Apps, such as Empower, can help you look at all of your investments at once to see how they're developing. Read more in our full review of Empower.

Risk: The chances you take with your money. It is the level of variability of your investments, which may go up or down. It could hurt or help your financial situation. - Less than 1 year = short-term goals

- Assess Your Ability to Take Risks

Your personality helps determine your risk level too. If you worry a lot, less-risky investments may be better. Obsessing over your investments isn't healthy. They may cause you to make rash decisions, affecting your finances. If, on the other hand, you don't worry much, more risk may work if you're okay with potential losses. Knowing you are in it for the long run may help.The best thing for most investors is to invest in a low-fee, broadly diversified, stock market index fund. Buying an individual stock is subject to tremendous risk. A mutual fund or ETF diversifies, and the volatility of that investment will be much less than that of the average single stock. A low-fee fund is essential, as that means more of the investor's hard-earned cash is being put to work. Just as stock market returns compound over time, the deleterious effects of high fees also compound over time.One good choice is the Vanguard Total Stock Market Index Fund ETF (Ticker symbol VTI). The fund is designed to track the performance of the Center for Security Pricing (CRSP) US Total Market Index, which represents approximately 100% of the investable U.S. stock market and includes large-, mid-, small-, and micro-cap stocks regularly traded on the New York Stock Exchange and NASDAQ. Total annual fund operating expenses are a miniscule 0.04%. So, for a $1,000 investment, $999.60 would be put to work and only $0.40 would go to fees. And there is no minimum investment required.

Robert R. Johnson, professor of finance at Heider College of Business, Creighton University, and co-author of Strategic Value Investing and Investment Banking for Dummies

In a perfect world, a balanced portfolio works best. It gives you a mix of risky and non-risky investments. When risky investments lose money, they can often be offset by more stable investments over time.

When to Invest: If you've got a big chunk of money gathering dust (and very little interest) in a traditional savings account, then investing in stocks or mutual funds may be right for you.But don't risk losing money you may need in the short term. Consider creating a rainy day fund first to cover unexpected expenses, including car repairs, illnesses, or even loss of a job. Or invest that money in a risk-free option like a high-yield savings account or CD.

- Evaluate the Fees

Most people investing $10,000 don't hire a financial advisor. The fees alone would eat away your profits. Instead, they handle their own investments. Even without a financial advisor, though, you may pay fees. Look closely at the fine print before choosing an investment.Fees you should watch out for include:

- Stock trading costs: Cost of buying or selling a stock

- Annual fees: Cost of holding an account with a particular company

- Account minimums: Fees you pay if you don't meet the required minimum

- Account maintenance fees: Fees to have your investment accounts at the financial institution

- Sales loads: Fees added to mutual funds upon purchase or sale (you should avoid these)

- Advisory fees: Annual fees paid to the investment professional assisting with your portfolio

- Expense ratios: Annual fees charged by mutual funds or ETFs, as a percentage of assets

- Stock trading costs: Cost of buying or selling a stock

Just as you might comparison shop for large ticket items, you should do the same for an investment firm. Ask about their fees. You may even be able to negotiate some of them.

Keep in mind, though, if you decide to change brokerage firms, you may face tax consequences. For more information on fees, see How to Invest Money.

If you are unsure about a brokerage firm, a great tool to use is BrokerCheck. They provide information about a broker's background, experience, and prior complaints.

2 Things You Should Do Before Investing

|

Before you jump right into investing your money, take inventory of your financial life. Ask yourself the following:

- Do you have a lot of personal debt?

- Do you have a 401(k)?

- Do you have an IRA?

You may want to get a handle on these things first. Here's how:

- Pay Down Your Debts

We don't normally think of paying debts down as investing. But it can be just as profitable, and sometimes more, in the long run. Here's an example:You can obtain a 5% rate of return on your investment portfolio. But you have $5,000 in credit card debt and you pay 23% interest.

If you invest your $10,000 rather than paying the $5,000 off, you actually lose 18% (= 23% - 5%). So paying off the credit card debt first is the smart move here. THEN you can invest the remaining funds using one of the strategies below.

Rate of return is the profit off an investment. Banks write it as a percentage. If you make $50 on a $1,000 investment, your rate of return equals 5%.Keep in mind that some interest is tax deductible. Credit card interest isn't but home mortgage interest is on the first $750,000. In this case, look at your after-tax rate of return to decide what to do. Here's an example:

You're in the 28% income tax bracket and pay a 5% mortgage interest rate. That means, you only pay 3.6% in mortgage interest after taxes (= 5% x (1 - .28)).

If you find an investment with a rate of return higher than 3.6%, then it makes sense to invest rather than pay down your mortgage. Once you pay down your debts, we recommend you focus on your retirement plans.

- Plan for Retirement

Ask yourself two questions:- Do you have a 401(k)?

- Does your employer match contributions?

First of all, if you don't have a 401(k), you should. This is especially important if your employer matches contributions.

Check with the HR department to see what percentage your company matches. Make sure to contribute at least that amount—otherwise, you're turning down free money.

401(k) Company Match: Some employer's VEST their contribution to your 401(k). This means you'll likely have to work a certain amount of time to receive a percentage (or the whole amount) of their match. But you'll ALWAYS get 100% of your contribution, regardless of how long you stay with the company.Even if your company doesn't match, consider contributing the maximum amount. It'll give your retirement savings a boost AND lower your taxable income.

You may also want to consider opening a traditional IRA or Roth IRA to supplement your long-term savings. Here are two situations to consider:

If you've maxed out your 401(k) contributions, you can put up to $6,500 ($7,500 a year for those 50 or older) post-tax in a Roth IRA annually.[5] And the best part is, you won't be taxed when you withdraw this money after retirement.

If you are self-employed, you could be eligible to open a Solo 401(k) or SEP IRA (Simplified Employee Pension). With a SEP IRA, you can contribute up to $66,000 per year.[6]

Check with a tax professional to review your options.

- Do you have a 401(k)?

One more thing. Before investing, you should have 3-6 months of expenses socked away in case you lose your job. Put it somewhere like CIT Bank. It is possible to build an emergency fund and grow your money at the same time.

Understanding Investing Risks

It's important to know the possible risks before choosing the right investment for you:

- Market risk: These are things you have no control over. If the overall financial market suffers, even diversification (basically having a balance of investments in your portfolio) doesn't eliminate risk.

- Business risk: If you invest in stocks, a company's corporate decision could affect your investment one way or the other. If the market perceives the decision as bad, the stock price could plummet.

- Political risk: Political events also may affect the market. Think about how the public reacts to major government events and decisions. These reactions can affect your investments, both foreign AND domestic.

- Liquidity risk: The time and cost involved in converting an investment into cash contributes to its risk. The more time or cost involved, the higher the liquidity risk.

- Concentration risk: The less diversified your portfolio, the higher your concentration risk. If you only hold two stocks and one of those plummets, your portfolio will take a big hit. But that's less likely if it's one plummeting stock out of 20.

Remember: The greater the possible reward, the higher the risk. When you take a loss, you'll need to decide whether to pull your investment or wait it out in hopes of reaping a higher return before too long.

What the Experts Say

As part of our series on saving and investing, CreditDonkey asked a panel of industry experts to answer readers' most pressing questions. Here's what they said:

Bottom Line

|

Your $10,000 has a promising future…as long as you have a smart plan to invest. Start by answering the following questions:

- Evaluate your situation: Do you have a retirement account? Do you contribute the maximum amount to it?

- Are you in debt? Is your interest rate higher than any rate of return you could get?

- Do you understand mutual funds, robo advisors, and stocks?

- Do you want to try something unique?

Knowing your situation will help you make a more informed decision. Many investment options have small minimum requirements and low fees. Shop around and consider your options to find the best way to grow your $10,000 investment.

Invest in Real Estate with $10+

- Only $10 minimum investment

- Get a diversified portfolio of real estate projects across the US

- Open to all investors

Invest in Real Estate with $100

- Short-term real estate investments lasting just 6-18 months

- Open to non-accredited investors

- Low fees

Invest in Rental Homes with $100+

Browse rental home investments for free. No bank account required

Start Investing in Real Estate

- Access to private real estate managed by experienced investors

- Earn passive income from dividends

- Open to all investors

J.P. Morgan Self-Directed Investing - Get Up to $1,000

- Get a cash bonus up to $1,000 when you open and fund a J.P. Morgan Self-Directed Investing account.

- $1,000 when you fund with $250,000 or more

- $325 when you fund with $100,000-$249,999

- $150 when you fund with $25,000-$99,999

- $50 when you fund with $5,000-$24,999

- Get the best of banking and investing on the Chase Mobile® app or Chase.com.

- Choose from stocks, ETFs (from index funds to cryptocurrency), options, mutual funds, money market funds, treasuries and more.

- Get unlimited commission-free online trades.

- Choose an account that's right for you: General Investing, Traditional IRA, Roth IRA, Trusts, or UTMA

- Access our secure, easy-to-use trading experience online or through the Chase Mobile® app.

- Our powerful tools and resources are built to help you take control of your investments.

- Rollover your retirement accounts and keep track of your investments in one place.

- Invest in S&P 500 and Nasdaq 100 stocks, or ETFS, from just $5 - trade from 7:30 AM to 5:45 PM ET for added convenience

INVESTMENT AND INSURANCE PRODUCTS ARE:

Deposit $100,000, get $1,000 in NVDA stock + 8.1% APY on uninvested cash

Terms and conditions apply

12 Free Fractional Shares + 1 Month Webull Premium

Make an initial qualifying deposit of $100 or more during the offer period to get 12 fractional shares and a 30-day subscription to Webull Premium. Maintain the initial qualifying deposit of $100 or more in the account for 10 days. Terms and conditions apply.

This offer has been collected independently by CreditDonkey. The details on this page have not been reviewed or provided by Webull.

Transfer and Earn Up to $5,000 Bonus

Enroll your new eligible TradeStation account in this offer either by using promo code BDEVAGFG on your new account application or by requesting to enroll, via telephone, with a TradeStation Representative. Within 45 days of account enrollment, fund your account with at least $500. Maintain at least $500 in your account for 270 calendar days. New assets will be aggregated during the 45-calendar day period following the enrollment date to determine the amount of your cash offer.

| New Assets | Cash Bonus |

|---|---|

| $500 - $24,999 | $50 |

| $25,000 – $99,999 | $250 |

| $100,000 – $199,999 | $400 |

| $200,000 – $999,999 | $800 |

| $1,000,000 – 1,999,999 | $3,000 |

| $2,000,000+ | $5,000 |

References

- ^ Fundrise, Explore client performance over time, Retrieved 8/29/2022

- ^ Investor.gov - Bonds, Retrieved 1/8/2021

- ^ Georgetown University, The Economic Value Of College Majors, Retrieved 1/8/2021

- ^ Zillow, What Does 'Normal' Home Value Appreciation Look Like?, Retrieved 1/8/2021

- ^ IRS, Retirement Topics - IRA Contribution Limits, Retrieved 7/19/2023

- ^ IRS, SEP Plan FAQs - Contributions, Retrieved 7/19/2023

Write to Kim P at feedback@creditdonkey.com. Follow us on Twitter and Facebook for our latest posts.

Note: This website is made possible through financial relationships with some of the products and services mentioned on this site. We may receive compensation if you shop through links in our content. You do not have to use our links, but you help support CreditDonkey if you do.

Fundrise, LLC ("Fundrise") compensates CreditDonkey Inc for new leads. CreditDonkey Inc is not an investment client of Fundrise.

Empower Personal Wealth, LLC (“EPW”) compensates CREDITDONKEY INC for new leads. CREDITDONKEY INC is not an investment client of Personal Capital Advisors Corporation or Empower Advisory Group, LLC.

|

|

| ||||||

|

|

|